by: Idris Mootee

While going through some my old files, I accidentaly discovered a small privately published book of DDB (now TBWA) in memory of 40th anniversary of the agency. Founded by Bill Bernbach (1911-1982), one of the early advertising legendaries of Madison Avenue. I remember it was given to me by then the president of the agency in 1989. It is a collection of his words.

"The magic is in the product"

"There are few things more destructive than an unsound idea persuasively expressed"

"Because an appeal makes logical sense is no guarantee that it will work"’

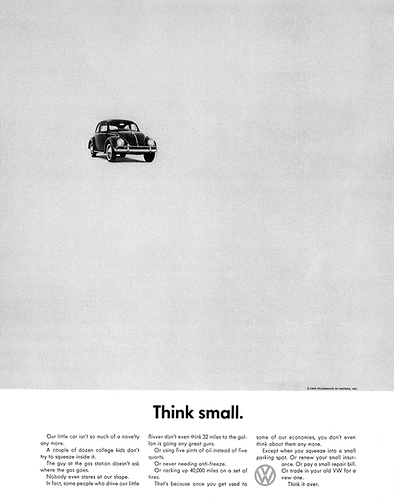

He started with 13 employees and a top floor office off Madison Avenue and the agency generated $775,000 during their first year in business. Whitey Ruben, owner of Levy’s Jewish Rye bread invited DDB to help their products. Their annual budget was less than $50,000; the agency viewed the account as its opportunity to gain attention in the Manhattan advertising community by introducing "ethnicity" into a marketing campaign. DDB’s Levy’s campaign ("You don’t have to be Jewish to love Levy’s") elevated the bread maker to the largest seller of rye bread in New York and helped Bill and his partners acquire the first of many big international clients. His VW ads were the most memorable and I considered them museum pieces.

He was a gentleman with brain and he represented the ideal image of an ad man/woman in those days. He was the ad man who brought "ethnicity" to advertising. Today, the industry is less glamorous and I am not too hopeful. Ad agencies used to be the marketing partners with their clients and all of a sudden that was evaporated. They have not stepped up and really added a strategic value component to the mix or simply big ideas. Instead, they are really becoming purveyors of low-cost advertising services.

Our friend David Armano asked me the question "Why do you think there are still so much consolidation and the demand for large marketing "engines"? There seem to be two competing models. Big one-stop shops or conglomerates and best of breed." This is a great question. Three big factors that drive consolidation: 1/globalization 2/integration 3/scale.

Globalization doesn’t need much explanation. Marketing campaign often run across divergent organizational cultures, making global account management more prevalent. There is still a need for better cost control and reporting. Clients want more visibility to agency costs. Agencies also need a clearer picture of their internal costs if they are going to maximize profits. More and more clients start seeing and buying ideas through the lens of strategic sourcing and procurement. Longtime relationships are being challenged as procurement departments take a hard look at what they get for their money. Commission-based fees are vanishing, replaced by fees based on agency costs.

Integration has always been a holy grail for advertisers. Imagine one firm that handles everything a client needs. With consolidation of the last ten years, I don’t see any progress. In fact it is more disintegrated because of the emerging of digital and social media. Scale has its advantages, but it will reach a point of diseconomy of scale. That’s when the scale advantage cannot make up for the additional cost of co-ordination and negative impact on the culture due to bureaucracy.

What is the future of advertising in the social-media and post-TV age and post agency mega consolidation? What would the next wave of consolidation be like? Will that extend to non-agencies acquisition? Or do we end up having only three agencies to pick from? More next week.

Original Post: http://mootee.typepad.com/innovation_playground/2008/01/what-is-the-fut.html

{kind=link}

{kind=link}