In 1997, a little known Harvard professor named Clayton Christensen published a surprise bestseller called The Innovator’s Dilemma, where he coined the term disruptive technology, which later evolved into disruptive innovation and became a mantra for the digital age.

Yet in a well argued piece in The New Yorker, his colleague at Harvard, the celebrated historian Jill Lepore, cries foul. She calls disruptive innovation a “competitive strategy for an age seized by terror.” “Transfixed by change,” she writes, “it’s blind to continuity.”

It’s not just Christensen’s theories that Lepore opposes, but what she calls the “rhetoric of disruption” which leads us to seek change for change’s sake, undermining productive stability. She also points out that disruption is no panacea and leads to failure more often than it does to success. So, is it time to rethink our culture of disruption?

Why Do Great Firms Fail?

To put Lepore’s criticisms in context, the best place to start is with Christensen’s initial idea. As a newly minted professor at Harvard, he became intensely curious about why great businesses fail. He wasn’t concerned with just any failures, but once high-flying firms with strong performance and great management. How did they lose their way?

What he found surprised him. The businesses he studied were following the many of the very same principles that his own institution espoused. They invested heavily in R&D, listened to their customers and relentlessly sought out markets with high profit potential.

His unlikely conclusion was that they failed not because they lost their way, but because they were following established practices. What he found was that in each case, the firm in question encountered something he called a disruptive technology. These had three common attributes:

They didn’t meet conventional performance standards: Customers tend to want better performance and businesses strive to continually meet higher standards. Yet Christensen found that as technology exceeded basic needs, an opportunity opened up for a product that actually performed worse by conventional metrics.

Lepore calls these “cheaper, poorer-quality products,” but that’s a common misapprehension. In many cases, they are cheaper, but they don’t have to be. Digital cameras, for example, were a disruptive innovation that was initially far more expensive than conventional cameras.

The important thing is that these innovations change the basis of competition towards new attributes. So they can be cheaper, but they can also be more convenient or offer other advantages not traditionally associated with the category.

They sold to less profitable markets: One of the things places like Harvard Business School has always drilled into their students was the importance of pursuing higher margins. Christensen found that disruptive firms often did the opposite. They actually targeted less profitable customers!

He offered steel minimills like Nucor as an example. In the beginning, they were only able to produce lower quality steel and the large integrated mills happily ceded the territory. By focusing on higher quality steel, the incumbents migrated upwards and actually increased their profitability initially.

However, as the minimill technology improved and the large integrated mills continued to migrate upwards and cede ever more territory, their business went into a tailspin. As Lepore points out in her article, they eventually recovered, but only after a long, painful period of reorganization.

They necessitated a change business model: Perhaps the most important aspect of disruptive technologies is that they require a change in business model. Kodak was unable to compete in the market for digital cameras not because it didn’t understand the concept (in fact, it helped invent it), but because the firm was making too much money selling film.

And that, in effect, is what makes disruptive technologies so difficult to deal with. They challenge incumbents to change not only their products and practices, but what they have come to value. If you’ve spent the last 50 years striving to make the world’s best film, it’s hard to embrace cameras that don’t use it.

Anatomy of Disruption

Lepore makes a valid point in asserting that we are too quick to glorify disruption. The Arab Spring has certainly disrupted the Middle East, but has yet to demonstrably improve the lives of the people in the region. I was excited to take part in the Orange Revolution in Ukraine, but disheartened by its aftermath. 10 years later, the country erupted again.

Yet Lepore veers off course by essentially affirming the consequent. She assumes that because disruption can often lead to poor outcomes, Christensen’s ideas are somehow at fault. In her fervent desire to critique, she conflates. Disruption, innovation and disruptive innovation are, in fact, three distinct entities.

As I’ve explained before, disruption is a function of networks. Innovation is a process of finding novel solutions to important problems. Disruptive innovation is not synonymous with either, but a special case of both. Essentially, it is a function of business processes and can only be adequately understood in that context.

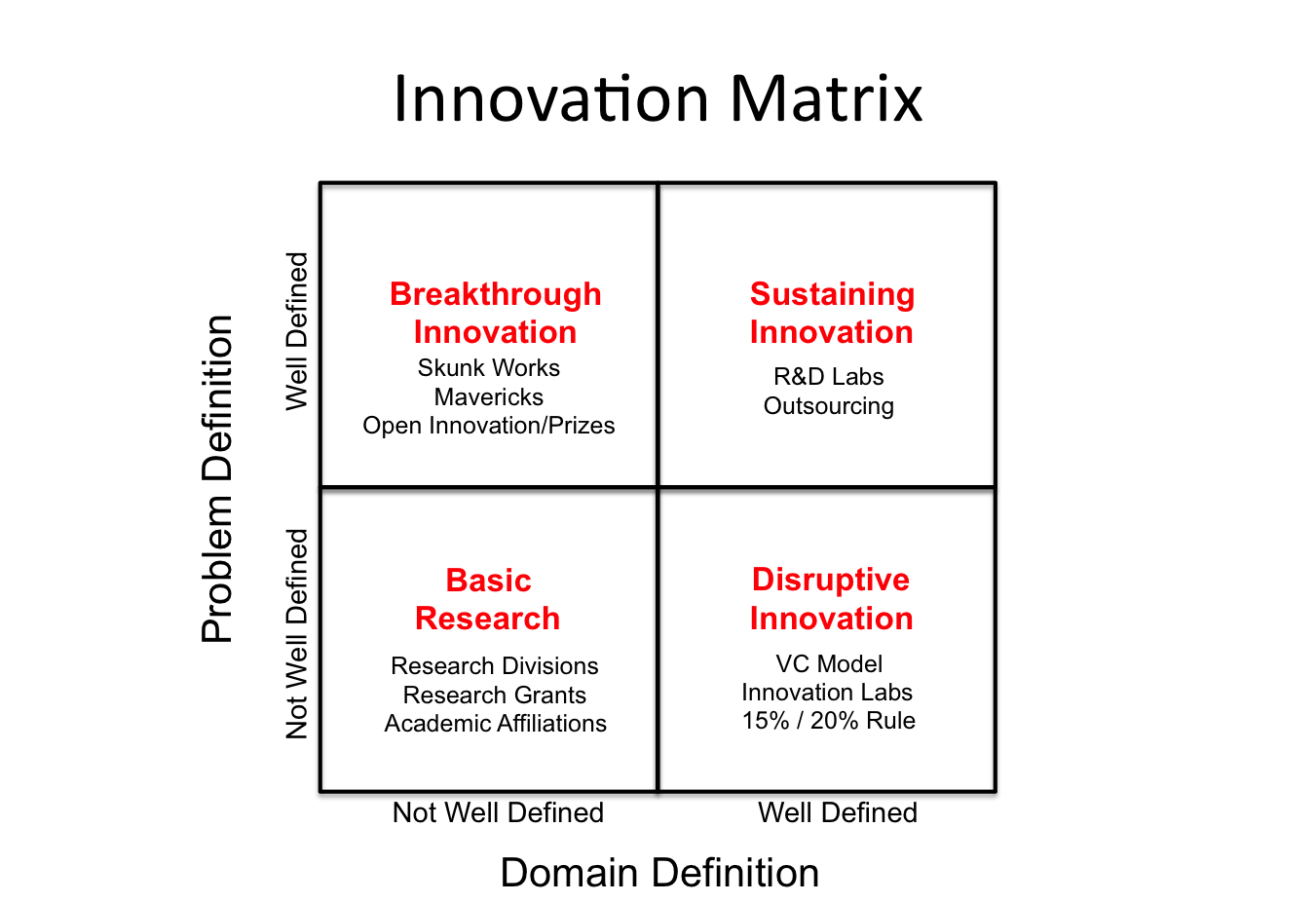

The Innovation Matrix

The constant juxtaposition of the terms disruption, innovation and disruptive innovation, makes for some very confusing semantics. Apple, for example, is certainly a disruptive company, but most of its products don’t meet the conditions described above. In fact, they are usually more expensive, perform better and employ conventional business models.

So in order to add some clarity, I developed the matrix below, first published in Harvard Business Review a few years ago.

Clearly, there is more than one way to innovate, what’s really important is the type of problem you are trying to solve. Apple, as I alluded to above, mostly attacks well defined problems in well defined areas and so focuses its efforts on sustaining innovation. Conversely, IBM spends a lot of money on basic research to push new frontiers.

That creates fundamentally different approaches to solving problems. For example, IBM maintains a large research division, but Apple does not. Other companies, like P&G, invest heavily in open innovation to solve well defined problems that they have become stuck on, but they feel will help them build better products.

Disruptive technologies are different mainly because it is difficult for incumbent businesses to develop them. They are, in effect, solutions looking for problems. They may present fantastic opportunities for VC firms that are willing to accept a high failure rate, much less so for existing firms who need to pay employees every month and keep the lights on.

Managing For Disruption

The subject of innovation is a somewhat technical one and its surprising to see Lepore pour so much vitiol into condemning it. What seems to offend her is not so much that a fellow professor wrote a book or that Silicon Valley hipsters hold conferences, but the glorification of disruption. She writes:

“A pack of attacking startups sounds something like a pack of ravenous hyenas, but, generally, the rhetoric of disruption—a language of panic, fear, asymmetry, and disorder—calls on the rhetoric of another kind of conflict, in which an upstart refuses to play by the established rules of engagement, and blows things up.

Yet despite her protestations, the world has clearly become more disruptive. Since 1960, the average lifespan of a company on the S&P 500 has fallen from more than 60 years to less than 20. Lifetime employment in one firm—or even one industry—has become a thing of the past (except, of course, for tenured professors at Harvard).

So although her objection to change for change’s sake is reasonable and even welcome, it’s not quite clear what she is advocating for, except perhaps to replace what she sees as blind obedience to disruption with blind obedience to continuity.

Like it or not, we can no longer assume stability, but must learn to manage for disruption. That does not mean that we need to kill all sacred cows, just that we need to constantly reconsider our devotion to them.

Original Post: http://www.digitaltonto.com/2014/is-disruption-dead/

{kind=link}